Cost analysis and optimization are central to effective business management, enabling organizations to understand cost structures, determine profit thresholds, forecast future expenses, and explain variances.

By distinguishing between fixed and variable costs, conducting break-even analysis, predicting cost trajectories, and analyzing actual vs. budgeted costs, businesses optimize profitability and operational efficiency.

Fixed vs. Variable Cost Analysis and Contribution Margins

Fixed costs are expenses that remain constant regardless of production or sales volume, such as rent, salaries, and insurance, while variable costs fluctuate with business activity, including raw materials, direct labor, and utilities.

The contribution margin, defined as the difference between sales revenue and variable costs, helps determine how much revenue contributes to covering fixed costs and generating profit.

Understanding the balance between fixed and variable costs supports more informed pricing, budgeting, and operational decision-making.

Break-Even Analysis: Determining Profitability Thresholds

Break-even analysis identifies the sales volume or revenue at which total costs equal total revenues, resulting in neither profit nor loss.

Formula (Units):

![]()

Formula (Revenue):

Application: Helps businesses understand minimum sales targets, assess pricing strategies, and evaluate project viability.

Example: If fixed costs are $60,000, selling price $300, and variable cost $200 per unit, break-even units = 600.

Cost Forecasting: Predicting Future Expense Trajectories

Cost forecasting uses historical data, trend analysis, and forecasting models to estimate future expenses, enabling proactive budgeting and effective financial planning.

It takes into account economic conditions, supplier price trends, and operational changes to provide a realistic view of future costs. By supporting scenario planning, cost forecasting helps businesses assess the impact of potential cost fluctuations.

Accurate forecasting minimizes financial surprises and guides strategic resource allocation.

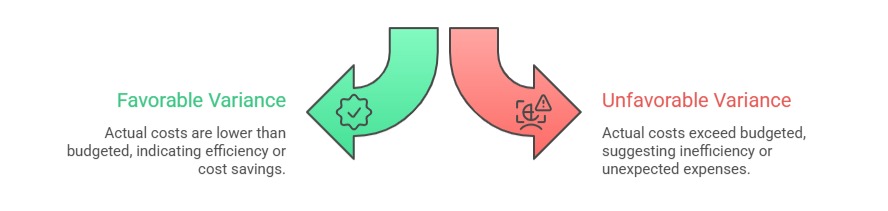

Variance Analysis: Explaining Differences Between Actual and Budgeted Costs

Variance analysis examines the differences between budgeted and actual costs to evaluate financial performance.

By identifying underlying causes such as inefficiencies, price fluctuations, or operational delays, variance analysis guides corrective actions and supports continuous improvement.

Ultimately, it enhances financial control, strengthens accountability, and helps organizations stay aligned with their budgeting goals.

Class Sessions

Sales Campaign

We have a sales campaign on our promoted courses and products. You can purchase 1 products at a discounted price up to 15% discount.